How Third-Party Lease Guarantors Work

Leap, Insurent and The Guarantors can back your lease when income or credit falls short. How the model works, what it costs, and which communities accept them.

You know exactly how frustrating the modern leasing process is. A single blemish on a credit report can derail an apartment application, leaving many wondering exactly how lease guarantors work.

Current 2026 market data shows property managers facing higher insurance costs. They are actively passing tighter screening rules down to renters. This makes approval harder than ever.

Our Houston Second Chance Apartments team was founded with a simple mission: to provide exceptional real estate locating services that customers can truly rely on. Everyday market conditions show us exactly where clients hit these roadblocks. We use specific tools to get those applications across the finish line.

Third-party corporate guarantors are often the deciding factor.

Let us look at the data, what it actually tells us, and explore how to use these services effectively.

The Basic Model of How Lease Guarantors Work

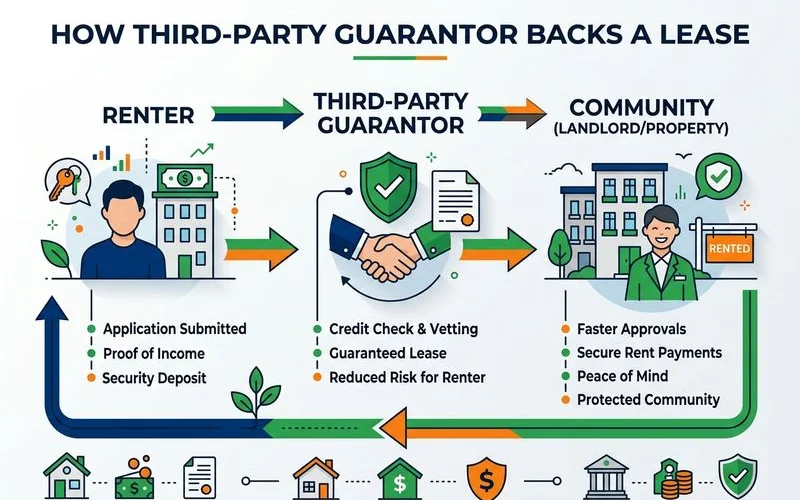

A third-party lease guarantor is a company that promises to pay your rent to the apartment community if you default. For the leasing office, that promise functions like a family co-signer with strong credit and income. The difference is that the company underwrites the risk.

You pay the guarantor company a non-refundable premium for this service. They review your application using automated risk models. We often see these companies issue approval decisions in under ten seconds.

Industry Insight: Institutional lease guarantees are backed by A-rated insurance carriers like AM Best or Argonaut Insurance Company. Landlords trust that institutional backing much more than a personal promise from a relative.

If approved, the guarantor signs an agreement directly with the apartment community. The community treats your application as if you had brought a strong personal co-signer.

If you pay rent on time, the guarantor never pays anything. Defaulting means they cover the obligation to the community and then pursue collection from you separately.

The Major Services in Houston

The Houston market relies on a few key institutional guarantors. Each service evaluates risk differently and partners with different building networks. We track these changing requirements daily to match renters with the right provider. A single application mistake can cost you money and time.

Leap

Leap is one of the most broadly accepted services for those seeking a leap guarantor apartment in Houston right now. They run a soft credit check that does not impact your FICO score. Fast approval usually happens within 24 hours.

Our team sees strong community acceptance for Leap at mid-range to premium properties. They are especially dominant in student housing through their Guarantor Waiver Program. Fees typically sit between 5% and 10% of your annual rent.

Best for: Renters with thin credit profiles but solid, verifiable income.

Insurent

An insurent guarantor policy is well-known at premium communities and corporate relocation contexts. Their underwriting is slightly more rigorous. They require a minimum income of 27.5 times the monthly rent.

This income threshold is significantly lower than the 40 times multiplier standard landlords demand. We know that their policies are fully secured by the Argonaut Insurance Company. Fees typically range from 70% to 110% of one month’s rent depending on citizenship status.

Best for: Higher-income renters aiming for luxury communities who just miss the strict standard income multiplier.

The Guarantors

Using the guarantors apartment service grants you access to a massive national network. Recent 2026 data shows they have over four million units enrolled nationwide. Broad Houston coverage exists primarily at mid-rise communities.

They use an AI-powered underwriting engine. This technology can process an application and return a decision in 9.6 seconds. We recommend them for renters who prefer an entirely online application process. Fees typically run 5% to 10% of the annual rent.

Best for: Renters who want the fastest, simplest online approval process.

Done Deal Cosign

Done Deal Cosign is far more flexible on second-chance applicants. They will work with renters who have prior evictions or broken leases. The company specializes in tougher cases that automated algorithms often reject outright.

Our experience shows they are willing to look at the full story behind a 500-level credit score. Fees vary widely by profile but frequently land between 7% and 12% of the annual rent.

Best for: Renters with severe rental history flags who need human underwriting.

Liberty Rent, Jetty, OneApp Guarantee

These newer entrants offer competitive fees and rapidly growing community acceptance. Jetty recently expanded its reach to serve over six million units nationwide through strategic partnerships. They are strongest at newer mid-rise and luxury properties.

Jetty provides flexible payment models. You can choose a low one-time premium or spread the cost into monthly payments. We find their fees typically range from 5% to 9% of the annual rent.

Best for: Profile-dependent applicants. We check the fit for these services on a case-by-case basis.

Eligibility Requirements

Most guarantor services require a baseline level of financial stability. They exist to lower the bar, not remove it entirely. We always verify your specific standing before recommending an application fee.

- Minimum income: Usually 27.5 times the monthly rent or 2 to 2.5 times the monthly rent. This is purposefully less than the standard 3x or 40x rules that property communities demand.

- Minimum credit score: Usually 580 to 630. A few specialized services will accept scores down to 500.

- U.S. residency: Most companies require legal U.S. residency or a valid U.S. visa.

- Employment verification: You must have active employment. Underwriters typically require your two most recent pay stubs from the last 30 days.

- No active bankruptcy: Most services immediately screen out applicants with active bankruptcies. The debt must be legally discharged.

Each service uses its own proprietary scoring model. We confirm your basic eligibility before you spend any money applying.

What It Actually Costs

Guarantor premiums vary based on the provider and your individual risk profile. Fees are generally non-refundable. You pay them directly at lease signing as part of your total move-in costs.

Our clients often ask for concrete numbers. For a $1,500 per month apartment, which totals $18,000 a year, you should expect the following estimated ranges based on current 2026 rates.

| Guarantor Service | Estimated Cost ($1,500/mo rent) | Pricing Model |

|---|---|---|

| Leap | $900 - $1,800 | 5-10% of annual rent |

| Insurent | $1,050 - $1,650 | 70-110% of one month’s rent |

| The Guarantors | $900 - $1,800 | 5-10% of annual rent |

| Done Deal Cosign | $1,260 - $2,160 | 7-12% of annual rent |

| Liberty Rent | $900 - $1,620 | 5-9% of annual rent |

| Jetty | $900 - $1,500 | Flexible monthly or one-time |

| OneApp Guarantee | $900 - $1,620 | 5-9% of annual rent |

We highly recommend factoring this premium into your initial apartment hunting budget. This prevents any last-minute financial surprises at the leasing desk.

How the Application Process Works

The exact sequence is critical for success. Applying to a community before you have guarantor approval can trigger an automatic denial. We guide renters through this specific pipeline to protect their application fees.

- Pre-screen your profile: We confirm which guarantor service fits your exact situation. Our database tracks exactly which Houston communities accept that specific service.

- Apply to the guarantor service: You will complete a secure online application. This usually takes 15 to 30 minutes. You must upload proof of income, a government ID, and sign a credit authorization. The Guarantors can issue a decision in under ten seconds, while others like Leap take 24 to 48 hours.

- Apply to the community: Submit the primary community application as usual. You must include the official guarantor pre-approval letter the service provides.

- Sign the lease: Pay the non-refundable guarantor premium at the time of signing. The guarantor agreement gets countersigned simultaneously with your lease documents.

- Move in: You pay your monthly rent normally. The guarantor policy simply remains as a silent backstop you never use unless you default on a payment.

When a Guarantor Service Beats Other Options

Paying a non-refundable fee is not ideal for anyone. Corporate guarantors offer distinct advantages when you analyze the math and the practical reality of renting in 2026. We look at three specific scenarios where this route makes the most financial sense.

- Guarantor Fee vs. Doubled Deposit: A guarantor fee is almost always cheaper upfront than paying a doubled security deposit. Tying up $3,000 in a refundable cash deposit severely restricts your moving budget. A $1,500 non-refundable guarantor premium keeps more cash in your bank account right now.

- Corporate Backing vs. Personal Co-Signer: Asking a family member to co-sign a lease places a heavy burden on that relationship. A corporate guarantor completely avoids those awkward financial conversations. We see many renters choose this option simply to keep their personal relationships free of financial obligations.

- Necessary Approval vs. Risk Fees: Many premium communities categorically refuse to charge simple risk fees for bad credit. They require an institutional guarantor policy instead. The corporate guarantor route becomes the only actual way to get the keys to those specific luxury units.

When a Guarantor Service Doesn’t Help

A corporate backstop is not a universal fix for every renting challenge. These services are highly specific tools. We actively advise against paying guarantor application fees in a few common situations.

- The community prohibits them: Some Houston properties strictly refuse all third-party guarantors. Property managers must explicitly opt-in to these programs. We will never waste your money applying to a building that rejects the policy.

- You fail the minimum requirements: If your credit score is 520 and the guarantor requires a 580, paying their application fee will not change the outcome. Algorithms instantly deny applications that fall below the hard floor.

- You have a willing personal co-signer: Free is always cheaper than spending $900 to $1,800. If a family member makes 80 times the monthly rent and will happily co-sign, you should take that route.

In these cases, you need a different strategy. Our team focuses on finding second-chance properties that evaluate your actual rental history instead of relying on third-party insurance.

A Real Houston Example

Comparing abstract numbers is helpful, but real-world scenarios show the true impact. Here is a typical profile we see in the Houston market.

The renter is applying for a $1,400 per month apartment. They have a 615 FICO credit score, a $3,800 monthly income, and a broken lease from 18 months ago that is fully settled.

Review exactly how different application strategies play out for this specific renter.

- Standard community application: The property manager denies the application. A broken lease combined with borderline income and thin credit triggers an automatic rejection.

- Standard community with a personal co-signer: The property manager approves the lease. This only works if the co-signer earns at least $112,000 annually and has excellent credit.

- Standard community with Leap: The community approves the application. The renter pays Leap an estimated $1,200 premium. Total move-in costs hit roughly $4,200.

- Second-chance-friendly community without a guarantor: The property approves the renter directly. They charge a $400 risk fee plus the standard deposit. Total move-in costs stay near $3,300.

The correct answer depends entirely on the specific building you want and the cash you have on hand. We run this exact math for every single client before they apply anywhere.

How to Move Forward

Now that you understand how lease guarantors work, handling the application process alone can be expensive and frustrating. We confirm your guarantor eligibility and match you directly to Houston communities that accept your specific service. The team coordinates the application timing to ensure you never waste a fee.

The entire locating service we provide to you is completely free. We get paid out of the property’s marketing budget, not your pocket.

Start your free guarantor-coordinated search or read who qualifies for a corporate co-signer in Texas to see your next steps.