Guarantor vs. Co-Signer: Which Does a First-Time Renter Need?

Guarantor or co-signer? They're not the same. Cost, role, and when each one fits a first-time renter.

We see the same hurdle every day with second-chance renters trying to overcome a past eviction or broken lease. Property managers will ask for financial backup, but mixing up the rules for a guarantor vs cosigner apartment application can ruin your chances. The difference between guarantor and cosigner dictates your legal risks, your upfront costs, and whose credit takes the hit.

Our team mapped out exactly how these roles function for applicants in 2026.

This guide explains what each role is and prepares you to secure an approval. The right financial backer turns an automatic rejection into a signed lease.

We will show you exactly how to choose the best path for your situation. Correct preparation is the key to securing better housing options. Your specific financial background determines the exact strategy you must use.

The Core Difference

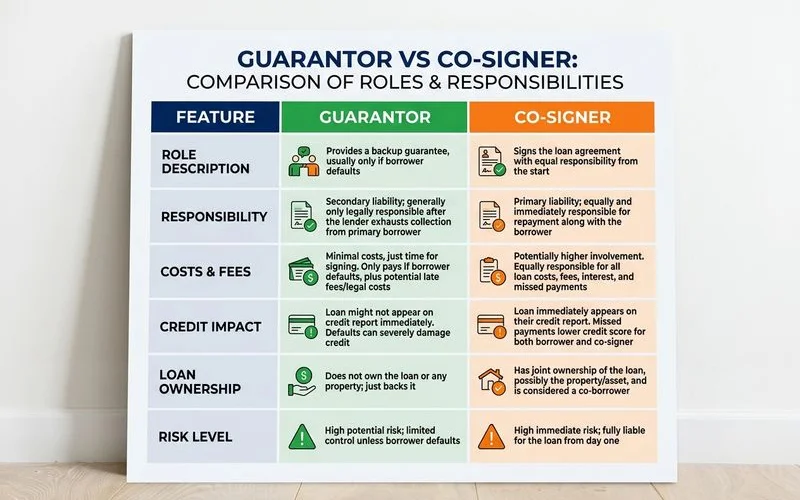

Our experts define a co-signer as a fellow tenant who lives with you, whereas a guarantor is an outside financial backer who lives elsewhere. A co-signer signs the lease and shares the space, while a guarantor only signs a separate financial agreement. The Texas Apartment Association (TAA) standard lease enforces “joint and several liability” for co-signers.

“Joint and several liability means the landlord can legally demand the entire monthly rent from either the primary tenant or the co-signer at any time.”

We remind clients that a guarantor does not have tenancy rights and cannot legally occupy the apartment. They simply act as an insurance policy if you default on the rent. The practical impact means your backer avoids nuisance complaints but still carries the financial weight.

Our leasing team often sees second-chance applicants assume a family member can just co-sign without moving in. Many Houston property managers reject that setup and require a formal Guaranty Agreement instead. Getting this detail right prevents instant application denials.

When Each Makes Sense

We recommend a co-signer when you plan to share the apartment, and a guarantor when you are applying solo but need income support. The choice depends entirely on who will actually occupy the bedroom. Each path solves a specific problem for renters with poor credit.

Co-Signer

Our leasing agents suggest using a co-signer in a few specific situations. Use a co-signer when:

- You are moving in with a partner or relative who will physically live in the unit

- You want shared legal responsibility and shared monthly rent payments

- The property allows combining incomes to meet the standard 3x rent requirement

- Your combined credit scores help offset a past bankruptcy or broken lease

A joint application often makes approval easier.

Guarantor

We prefer guarantors for solo applicants facing credit hurdles. Use a guarantor when:

- A wealthy relative wants to secure your approval but refuses to be listed as a tenant

- You are renting a $1,500 Houston apartment alone and cannot prove $4,500 in monthly income

- The community requires a clean separation of liability without involving the backer in daily property rules

- Your backer wants to avoid liability for property damages caused by your guests

This structure protects the backer from daily leasing disputes.

Personal vs Corporate

Our platform categorizes backers into two camps: personal contacts who help for free, and corporate insurance companies that charge a premium. A personal backer uses their own wealth, while a corporate service issues a surety bond to the landlord. Both options provide the financial security that property managers demand.

Personal Co-Signer or Guarantor (Free, Usually)

We see clients use personal guarantors to bypass strict second-chance property algorithms. A family member with excellent credit can vouch for you without any upfront fees. The trade-off involves placing a heavy financial burden on someone you love.

Our team tracks Texas community standards, and most require personal guarantors to meet very high thresholds. If you face another eviction, the property management company will sue your family member for the balance. Standard requirements in 2026 typically include:

- A FICO credit score of 700 or higher

- Gross monthly income equal to 4x or 5x the rent (e.g., $6,000 to $7,500 monthly for a $1,500 apartment)

- Stable U.S. residency and verifiable, long-term employment

- Willingness to upload sensitive tax returns and pay stubs to a third-party portal

Corporate Guarantor Service (Fee-Based)

We rely on corporate services when an applicant’s family cannot meet the 5x income multiplier. Companies like TheGuarantors, Insurent, Rhino, and Leap sell lease guarantee bonds directly to the property. You pay a non-refundable premium, and the company guarantees your lease to the landlord.

Our agents tell applicants to budget between 5% and 10% of the annual rent for this service. There is no “corporate co-signer” option, because these businesses never sign as tenants. For a $1,500 per month Houston apartment ($18,000 annually), the fee ranges from $900 to $1,800.

We partner with TheGuarantors because they often offer more flexibility for renters rebuilding their credit after a bankruptcy. Insurent currently requires applicants to prove 27.5x the monthly rent in annual income or hold 50x in liquid assets. Paying this fee secures your approval without straining personal relationships.

Cost Comparison

We break down the costs by showing that personal options are free, whereas corporate guarantors require a massive upfront payment. The table below highlights the financial and legal differences side-by-side. Reviewing these facts helps you plan your move-in budget accurately.

| Feature | Personal Co-Signer | Personal Guarantor | Corporate Guarantor |

|---|---|---|---|

| Direct cost | Free | Free | 5-10% of annual rent ($900-$1,800) |

| Living arrangement | Lives in the unit | Lives elsewhere | N/A, corporate entity |

| Legal status | Tenant on the TAA lease | Guarantor only | Guarantor only |

| Credit impact on backer | Yes (shows as active debt) | Sometimes (depends on the screening tool) | None, they are a corporate service |

| Approval timeline | Processed with your application | Processed with your application | Usually 24-48 hours separately |

Tax and Credit Implications

Our experts warn clients that a co-signed lease appears directly on the backer’s Equifax or Experian credit report as an active financial obligation. A standard guarantor agreement typically stays off the report unless a default goes to collections. This distinction severely impacts a backer’s debt-to-income (DTI) ratio.

We see this ruin family mortgage applications when the parent tries to buy a new house. If a parent co-signs your $1,500 apartment, mortgage lenders will count that $1,500 against their monthly liabilities. A personal guarantor avoids this daily DTI hit, keeping their credit profile cleaner.

Our advice is to always protect your backer’s credit score by understanding the risks. Key credit facts to keep in mind include:

- Co-signing adds the total rent amount to the backer’s credit report

- Guaranteeing only impacts credit if the debt goes to a collection agency

- Defaulting on the rent will destroy the credit profile of everyone involved

- Hard inquiries occur for both roles during the initial background check

Property managers will file an eviction against both parties if the balance remains unpaid.

Common First-Time Renter Scenarios

We match your specific background issues to the most cost-effective backer strategy. A recent bankruptcy requires a very different approach than a simple lack of rental history. Reviewing these common profiles will help you identify your best move.

Scenario 1: Parent Willing to Help, Lives Across Town

Our agents recommend a personal guarantor when the parent meets the strict 5x income rule but stays at their own residence. Best fit: Personal guarantor. They sign the TAA Guaranty Agreement, provide their W-2s, and pay zero fees.

Scenario 2: Moving in With Significant Other With Strong Credit

We combine both incomes to hit the standard 3x rent threshold for joint tenants. Best fit: Co-applicants (technically not a co-signer scenario, as both apply as joint tenants). Both individuals share the apartment, and both carry joint liability for the monthly payments.

Scenario 3: Family Cannot Help Due to Poor Credit

Our second-chance renters use companies like TheGuarantors to bypass family involvement entirely. Best fit: Corporate guarantor service. You pay the $1,500 premium upfront, and the property gets the insurance bond they demand.

Scenario 4: Just Need a Small Boost After a Broken Lease

We often negotiate an extra month’s rent as a security deposit for clients with a single broken lease. Best fit: Higher deposit instead. The Texas Property Code allows landlords to hold larger deposits to offset risk.

Our leasing strategy relies on this because you get the money back at move-out. This approach costs the same upfront as a corporate fee, but acts as a refundable safety net. Many smaller landlords prefer this extra cash over a corporate bond.

How to Choose

We use a simple decision tree to help applicants bypass automated rejections. Answering these four questions narrows down your exact path if you are wondering, ‘do I need a cosigner apartment?’ This process prevents you from wasting application fees on properties that will deny you.

Our team suggests asking these questions before touring any property:

- Can I qualify on income alone? If yes, you do not need any external backing.

- Do I have a family member with a 700+ credit score willing to back me? If yes, ask them if they prefer the co-signer (shared tenancy) or guarantor (financial only) route.

- Will the property accept a corporate guarantor service? Many 2026 Houston properties accept Rhino or TheGuarantors, but strict luxury buildings might decline them.

- Would a higher deposit be cheaper than a guarantor fee? Offering a double deposit is usually smarter for short-term leases, since the money is refundable.

Taking these steps clarifies your true move-in budget. The right answers keep you from dropping $100 on a background check at a building that refuses corporate guarantors.

We confirm a property’s exact criteria before you spend any money on application fees. Knowing the property rules beforehand is the key to second-chance renting. Property managers respect applicants who come prepared.

How to Move Forward

We pre-screen Houston apartment communities to verify exactly which guarantor types they accept for applicants with bad credit. Solving the guarantor vs cosigner apartment dilemma based on your specific credit profile saves you time and money. You can read about how third-party lease guarantors work to understand the backend process.

Our agents are ready to help you handle the entire leasing process.

Simply Start your free first-time renter search to get a customized list of approving properties. Securing a great apartment is absolutely possible with the right preparation.